Summary: Today we have a quick look at the US economy. Where it’s at. Grading its performance. Where it’s going.

.

Contents

- The slow growth recovery

- Good news!

- Bad news!

- Perhaps very bad news: are we like Japan?

- The clock runs against us

- For More Information

.

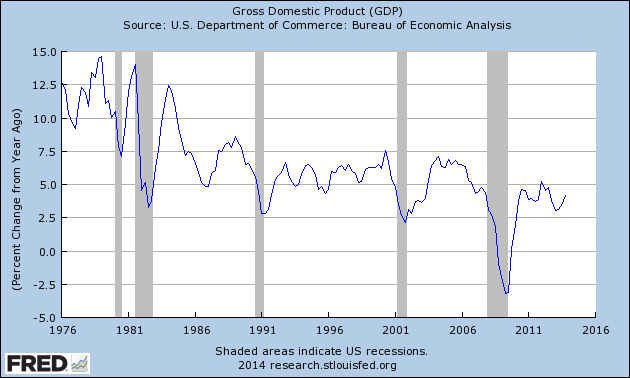

(1) The recovery: slow steady growth

Before looking ahead, let’s look back. In November 2012 the consensus estimate of 2013 real GDP was 2.3% (Wall Street Journal survey of economists). Based on the preliminary estimates of Q4 GDP, current estimate of 2013 GDP is 2%, as of Friday. That’s reasonably close.

Is 2% good or bad? Context matters.

- 2% growth would be horrific for China with potential growth of 5% – 7%, per capita of $6,500.

- The US has grown at 2.2% since 2010, only slightly below the Fed’s 2.2% – 2.4% estimate of long-term GDP growth (a slowing from the post-WW2 average). So 2% is a disappointing slowdown.

- On the other hand, 2% is slow for a recovery, especially following the deepest recession since the 1930’s.

Worse, the trend of GDP has an ugly look. Real GDP might be stabilizing at a lower level of growth. For the second time. The first slowing was after 1980 (the oddly named “Reagan Revolution”).

.

But real GDP is not always the relevant number. In many ways we living in a nominal world. Profits, savings and many important factors require nominal growth. Unfortunately, the nominal graph looks similar to the graph of real GDP.

.

.

(2) Good news

The second half of 2013 was strong: the fiscal deficit fell, the job picture improved (e.g., falling new claims for unemployment insurance, steady growth in the number of new jobs), with strong growth in construction, manufacturing and exports.

Economists expect 2014 to be the year in which the US economy shifts into high gear. The consensus forecast is 2.8% (Wall Street Journal Survey). It will be a year of “Red, White, and Boom” (BofA), in which it reaches “escape velocity”.

If so, the government’s fiscal and monetary policy will have succeeded in supporting the economy until normal growth recovered.

On the other hand, even growth of 2% is adequate — if disappointing compared what America could do if better managed.

(3) The bad news

After a strong second half in 2012, the economy appears to have slowed in December. New orders in December’s durable goods report were down 4.3% (SA). December’s vehicle sales and housing data were also weak — both have risen for several years on low credit standards and low rates, drivers that now might be reversing. Some of this might have been from the weather. Update: January vehicles sales were also down.

Also, the turmoil in the emerging nations seems likely to depress 2014 exports.

Continued slow growth (~2%) in 2014 would be significant for several reasons.

- The inability to accelerate since 2010 decisively above 2%, despite years of stimulus, suggests some underlying problem in the US economy.

- Slow growth provides only a small cushion against shocks that can knock the economy into recession.

- Some economists believe the economy has a “stall speed” of ~2% (“Forecasting Recessions Using Stall Speeds”, Jeremy J. Nalewaik, April 2011), below which it falls into recession. Perhaps that’s why the Fed injected stimulus whenever growth fell below 2%. If so, slowing could pitch the economy into a recession.

Why so much worry during the past three years about a recession? With our high unemployment, moderately high fiscal deficit, and the Fed already running ZIRP & QE — we are weak and have relatively little capacity to fight a recession. A recession could quickly become very painful.

What comes next? We only know where the economy was a few months ago. Friday’s employment report will tells much about jobs and wages in January; the data in the next few weeks will tell us more.

(4) Perhaps very bad news: are we like Japan?

Japan has been in a slump since 1989, growing at ~1.1%/year. And that slow growth came from decades of zero interest rates and massive fiscal deficits (mostly wasted spending) — plus from exports, before so many nations seized upon exports as the key to growth

This has left Japan with enormous levels of government debt, so that a mistake or bad luck might cause economic disaster or een political regime change. It’s not a comforting example, except for believers in Modern Monetary Theory.

For more about this see: “Is America Turning Japanese?“, Brad Delong (Prof Economics, Berkeley), Project Syndicate, 30 January 2014.

(5) The clock runs against us

Context matters in another way. The US has had periods of economic stress before. For example, the great inflation of the 1970s, followed by the Volcker shock of 1980 – 1983. But America today differs in two great ways from anything in the post-war era:

- Those were years of debt accumulation, providing a strong steady wind at our backs.

- Those were the years of the boomers growth and maturity, another steady wind in our sails.

Both those trends are exhausted, and reversing. The younger generations have lower income growth than the boomers did at that point in their lives, with more debt from college. Meanwhile the boomers’ years of borrowing and accumulating goods are behind them. Worse, they enter retirement with astonishingly high levels of debt and low savings. For most retirement means a large drop in spending.

A few years of spending growth would better launch the younger generations and allow boomers to build savings before retirement.

There is a silver lining. Structural reform to our health care system (copying the best features of our peers’ systems) could pay large benefits to America. And looming ahead is the Third Industrial Revolution; the resulting boost to productivity erase many of our problem disappear (assuming we manage to distribute its bounty).

(6) For More Information

(a) Posts about the economy about…

(b) Posts looking at the economy today:

- Rising consumer debt driving the recovery: boon or bane?, 10 November 2013

- Larry Summers gives us the bad news. Worse, the only solution is more of the same., 20 November 2013

- The astonishing news about the December jobs report: it shows continued slow growth, 13 January 2014

- The state of the American middle class: are we thriving or sinking?, 15 January 2014

(c) Other posts about the consequences of our deficits:

- America is rich and powerful because we can borrow. Will this debt build a stronger America?, 5 June 2012

- America’s strength is an illusion created by foolish borrowing, 10 October 2012

(d) About monetary policy

- Do you look at our economy and see a world of wonders? If not, look here for a clearer picture…, 21 September 2013

- The great monetary experiment enters a new phase, with America as the stakes, 27 October 2013

- The key to understanding the future of QE3, and the future of our economy, 12 November 2013

- Has the Fed blown another housing bubble?, 30 January 2014

- A Fed Governor speaks honestly to us about the costs and risks of our monetary policy, 18 January 2014

.

.