Summary: Many US economic indicators have fallen off their peaks, some entering typical pre-recessionary levels. That’s bad, since the fiscal deficit and unemployment are already at recessionary levels. That’s a ugly place to start the downturn. And the it might have already begun.

Contents

- The ECRI says the recession began in July

- About the ECRI

- Economist Gary Shilling also sees a recession

- Updates

- About Economic Statistics & Forecasts

- For More Information

(1) ECRI: the recession began in July 2012

The ECRI is one of the leading US economic forecasting groups. This is a follow-up to their prediction of recession in 2012 made in September 2011, described here.

———————-

“The Tell-Tale Chart”

Excerpt from a press release of the Economic Cycle Research Institute (ECRI), 29 November 2012.

Following our September 2011 recession call, we clarified its likely timing in December 2011. Based on the historical lead times of ECRI’s leading indexes, we concluded that, if it didn’t start in the first quarter of 2012, it was very likely to begin by mid-year.

But we also made it clear at the time that you wouldn’t know whether or not we were wrong until the end of 2012. And so it’s interesting to note the rush to judgment by a number of analysts, already asserting that we were wrong.

So, with about a month to go before year-end, what do the hard data tell us about where we are in the business cycle? Reviewing the indicators used to officially decide U.S. recession dates, it looks like the recession began around July 2012. This is because, in retrospect, three of those four coincident indicators – the broad measures of production, income, employment and sales – saw their high points in July (vertical red line in chart), with only employment still rising.

.

FM Note: for more detailed versions of these charts see this page by the St. Louis Fed.

But if we’re in recession, and the business cycle peak was in July, how could employment be higher three months later? Actually, this was also true in three of the last seven recessions – and in the severe ’73-’75 recession, job growth stayed positive eight months into the recession. Thus, positive jobs growth isn’t inconsistent with the early months of recession. Of course, all of this data is subject to revision, but, as we’ve noted before, the ultimate revisions to coincident indicator data after business cycle peaks tend to be downward.

If you look at the size of the simultaneous declines in industrial production and personal income since July, that combination has never occurred outside a recessionary context in over half a century – but it’s occurred in every recession. This leads us to conclude that we are most likely already in a recession that began around mid-2012.

Now, please remember that, following our recession call, central banks really ramped up their efforts, and have literally been pumping more money into the economy than at any time in the history of humanity – and this is the upshot. No wonder the Fed is now all in.

So how come hardly anybody recognizes the recession? Perhaps it’s because of real-time data showing positive growth in GDP and jobs, and the lack of a recent salient shock.

Many believe a major negative shock is necessary to start a recession. But think back to the big shocks in the last two recessions. The 9/11 attacks were widely believed to have triggered the 2001 recession that had really started six months earlier. And many thought that the financial turmoil set off by the Lehman Brothers failure caused the 2007-09 recession that had actually begun nine months earlier. At the time, with seemingly positive – indeed strongly accelerating – GDP growth in the first two quarters of 2008, most didn’t realize that a recession was already in progress when Lehman collapsed. …

———————-

A note about the ECRI’s chart: Industrial production and personal income rolled over in July. Sales depend on Xmas. Employment is a lagging indicator, last to inflect.

(2) About the Economic Cycle Research Institute

The ECRI is an independent research institute. Their indicator systems predict the timing of changes in an economy’s direction, before the consensus of economists.

The ECRI’s co-founder was Geoffrey H. Moore. From his March 2000 NY Times obituary ”In a sense, he was the father of the leading indicators as we know them today,” said Anirvan Banerji, co-director of research with Dr. Moore at the Economic Cycle Research Institute. The successor to the forecasting tools he developed is ECRI’s Weekly Leading Index (WLI).

From 1949 to 1978 Moore set the start and end dates of recessions for the National Bureau of Economic Research (NBER). When they created a committee for this, he was its senior member. Using the same approach, ECRI has long determined recession start and end dates for 20 other countries that are widely accepted by academics and major central banks as the definitive international business cycle chronologies.

For information about their approach, see their About page.

(3) Economist Gary Shilling also sees a recession

Videos:

- He expects a recession in 2012, Bloomberg TV,

13 April 2012 - He says the US recession began in the second quarter, Yahoo, 13 August 2012

- His current forecast, Bloomberg TV, 12 November 2012

For more about Gary Shilling, see Wikipedia.

(4) Updates

(a) John P. Hussman, manager of the Hussman Funds, believes that “U.S. economy joined a global economic downturn during the third quarter of this year.” Hussman is a former professor of economics and international finance at the University of Michigan. Source: his weekly market comment, 3 December 2012.

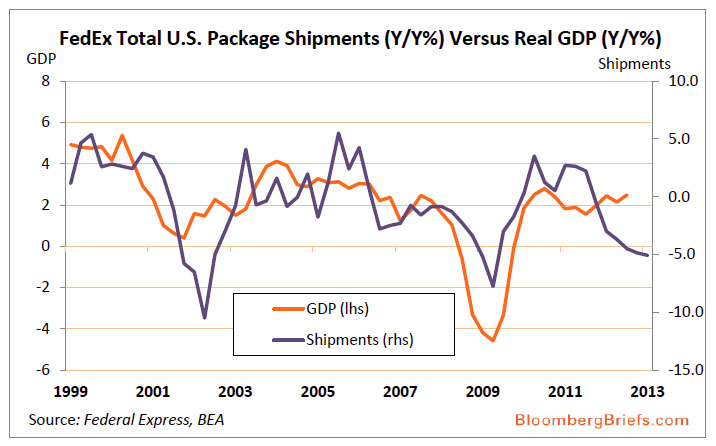

(b) Another straw in the wind

Remarks by Fred Smith, the CEO of FedEx , on their quarterly conference call, 18 Spetember 2012 (from Seeking Alpha):

…fundamentally, what’s happening is that exports around the world have contracted, and the policy choices in Europe and the United States and China are having an effect on global trade. Global trade has grown faster than GDP, except for the 2000, 2001 meltdown and 2008 and 2009, for 25 years. And over the last few months, that has not been the case. So that’s what’s really going on, is that exports and trade have gone down at a faster rate than GDP has.

Today from Bloomberg Briefs (subscription only):

“The level of FedEx package shipments began to slump as early as the first quarter of 2012 and now appears to be signaling weaker economic conditions for 2013.”

.

.

(5) About Economic Statistics

Economic statistics work for us like the whiskers on a cat. As we move into the unknown future, they hint at what lies ahead. Nobody can say what comes next — economic science is immature, the data too poor — but ignoring the data is imprudent, even foolish. Here are the key things we know.

(a) US recessions are defined by the National Bureau of Economic Research (NBER) as follows:

A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. … Most of the recessions identified by our procedures do consist of two or more quarters of declining real GDP, but not all of them.

… Our procedure differs from the two-quarter rule in a number of ways. First, we consider the depth as well as the duration of the decline in economic activity. Recall that our definition includes the phrase, “a significant decline in economic activity.” Second, we use a broader array of indicators than just real GDP. One reason for this is that the GDP data are subject to considerable revision. Third, we use monthly indicators to arrive at a monthly chronology.

(b) The US economy very seldom rolls over quickly, except from an external shock (e.g., the 1973 oil embargo, 2007 real estate bust). The US economy is a $15 trillion ship. It turns only slowly.

(c) The recession could have already started and we might not know it yet. A recession typically means that GDP declines by 2% (plus or minus) per year. We can no more detect that by our personal experience than we can sense a slow 2% change in the air temperature. These things are visible only in the macroeconomic data.

(d) Since the “real time” economic data is hideously unreliable (subject to large revisions many months later), recessions are determined well after the fact. Most current economic numbers (before revisions) are unreliable for three reasons.

- We have a large, complex, and constantly evolving economy — all of which make it difficult to measure (or even devise metrics).

- Most economic metrics are abstractions. Measuring GDP, personal income, or inflation is not like counting apples.

- The government statistical apparatus is grossly underfunded. We get the economic statistics we pay for.

(e) Economic theory is improving, but as yet still immature (as are all the social sciences). Economists have learned much during the past few centuries, but reliable forecasts remain beyond the state of the present art.

(f) As a result of these things, the consensus forecast of economists, as measured by the Blue Chip Financial Forecasts and the Wall Street Journal’s Economic Forecasting Survey, have never successfully predicted a recession.

(6) For More Information

Lessons learned by looking back at the last recession: Making us dumber, chanting “Dude, where’s my recession?”, 3 June 2008 — We were in a recession, which Republicans could not believe or accept (see the comments).

Looking ahead, this was written two months before the ECRI’s start date of the new recession: A status report about the US economy (we party so hard we cannot hear the alarms ringing), 27 March 2012.

Other posts looking at the US economy:

- It’s the end of the world we’ve known since WWII (updated status report), 29 June 2012

- About the October jobs report: new jobs, bought at great cost, 2 November 2012

.

.

“The government statistical apparatus is grossly underfunded. We get the economic statistics we pay for.”

Are there any nations where this is not the case? I think it would be useful to compare the ‘fundedness’ of econ statistics vs how quickly these nations’ governments acted to shorten a downturn vs how effective it was.

“I think it would be useful to compare the ‘fundedness’ of econ statistics vs how quickly these nations’ governments acted to shorten a downturn vs how effective it was.”

That would be useful and interesting! But that measures the political response to an economic downturn. A more focused measure would be the size and speed of revisions to economic data. Large, slow revisions show underfunding of the economic sensory machinery.

Employment is well known to be a lagging indicator, ditto measures of GDP growth, which are usually cumulative aggregate numbers revised after the fact to take into account many complex dynamics of the modern industrial economy, such as seasonal adjustments, etc.

Modern economies are enormously complex systems with many moving parts, and a snapshot in time gives only a bare glimpse of the fuzzy outlines of what’s going on. People speak about “the fog of war,” but they really ought to talk about “the fog of a modern economy.” Keynes-Wickell-Fisher macroeconomics offers a broad general guide (viz., DON’T cut government spending in the midst of a major recession; DO try to balance the budget in the midst of an economic boom), but cannot tell us specifics like what quarter the economy slipped into a recession, or what next quarter’s GDP will be.

Remarks by Fred Smith, the CEO of FedEx, on their quarterly conference call, 18 Spetember 2012 (from Seeking Alpha):

Today from Bloomberg Briefs (subscription only):

.