Summary: Al Qaeda (Bin Laden’s organization, if it still exists in meaningful form) is a threat to America. A greater threat are our CEO’s, some of whom who have discovered discovered a formula to vast personal wealth: leverage the company up (borrow), use those funds to buy back stock (boosting earnings per share), cut capital expenditures (capex) to boost short-term profits, pay most of the profits in dividends — all of which disguises massive payouts to senior managers (via salary, benefits, pensions, golden parachutes, grants of stock and stock options, etc). They’re strip-mining away America’s future. Slowly people begin to fit these pieces together. Today we help you to do so.

.

Contents

- An example of how it’s done

- Cutting capex: short-selling the future

- For More Information

.

(1) An example of how it’s done

List most stories about corporate finance, it’s complex. These articles clearly explain the game using IBM as an example (just one of many), but have to be read. The excepts are just teasers.

(a) “Stockholders Got Plundered In IBM’s Hocus-Pocus Machine“, Wolf Richter, Testosterone Pit, 17 October 2013 — Opening:

I’m not picking on IBM. I’m almost sure they have some decent products. So they had a crummy quarter – the sixth quarter in a row of sales declines. And their hardware sales in China have collapsed since Snowden’s revelations about the NSA and its collaboration with American tech companies. But in one area, IBM excels: its hocus-pocus machine.

IBM isn’t alone in its excellence and isn’t even at the top of the heap in that respect. There are many corporations like IBM, mastodons that successfully pull a bag over investors’ heads, aided and abetted by Wall Street with its “analysts,” and by the Fed, to hide the stockholder plunder taking place behind a billowing smokescreen of verbiage.

(b) “Big Blue: Stock Buyback Machine On Steroids“, David Stockman, at his website Contra Corner, 17 April 2014 — Opening:

The Fed’s financial repression policies destroy price discovery and honest capital markets. In the process these deformations turn financial markets into casinos and corporate executives into prevaricating gamblers. To be specific, most CEOs of the Fortune 500 are no longer running commercial businesses; they are in the stock-rigging game, harvesting a mother lode of stock option winnings as the go along.

Those munificently rising stock prices and options cash-outs owe much to the Fed’s campaign to suppress interest rates and fuel stock market based ”wealth effects”, but the CEOs are doing their part, too. They have become full-time financial engineers who use the Fed’s flood of liquidity, cheap debt and soaring stock prices to perform a giant strip-mining operation on their own companies. That is, through endless stock buybacks and M&A maneuvers they create the appearance of “growth” while actually liquidating the balance sheet equity and future asset base on which legitimate earnings growth depends.

.

The poster boy for this deformation is IBM which for all intents and purposes has become a stock buyback machine on steroids. It had a bad hair day yesterday, reporting still another year/year decline in sales, but that goes right to the heart of the matter. During the last seven years IBM has been a stock traders dream, climbing an almost picture perfect chart from $94 per share in March 2007 to a recent peak of $212.

But as shown below, those gains had nothing to do with what has been a historic ingredient of stock appreciation—- namely, expansion of its asset base and revenues. In fact, sales revenues in Q1 2014 clocked in at virtually the same number as Q1 2007 …

(c) “The Great Stock Buyback Craze Is Finally Ending“, Zero Hedge, 17 April 2014 — Opening:

… as we forecast first in 2012, all that investment grade companies like IBM have done in the New Normal in order to preserve the illusion of growth, is to use cash from operations, or incremental zero-cost leverage, to fund stock buybacks with the express goal of reducing the number of shares, and hence dilution, in the EPS calculation. In essence a balance sheet for income statement tradeoff. Earlier today, David Stockman touched just on this issue.

However, that “great stock buyback craze” as we call it, is finally coming to an end. Why?

Before we explain, in order for readers to get a sense of the true perspective of how massive IBM’s stock buybacks have been over the past two years, here is a chart showing the quarterly amount of net debt issued by Big Blue as well as the total notional in stock buybacks.

(d) “Cash Does Not Mean Capex, IBM Edition“, Jeffrey P. Snider, Seeking Alpha, 17 April 2014

Related to yesterday’s observations about corporate cash, the broken record of IBM (IBM) revenue continues to demonstrate the unwillingness of American businesses to freely spend on capex.

(2) Cutting capex: short-selling the future

What America’s corporations are not doing: investing in their businesses. Cutting capex means big profits in the present — and big paychecks for the senior executives — but a weak future for the company. It’s just one ill consequence of the paradigm for the successful modern American CEO.

(a) “Ending corporate America’s investment drought“, Financial Times, 23 January 2014 — Opening:

If 2014 is the year the US economy finally picks up speed, it ought to be the moment companies start investing. US non-financial companies are sitting on record levels of cash – almost $1.5tn. Alas, there is scant sign that chief executives are preparing to put their balance sheets to better use. The latest survey of non-financial companies in the S&P 500 index shows they are expected to boost capital expenditure by just 1.3 per cent for the year ending in June, according to Factset, a data company. This hardly looks like a vote of confidence in the US recovery. Unless companies show signs of stepping up their investments, there will be a question mark over its sustainability.

(b) “Don’t Blame Regulation For Capital Spending Drought“, Martin Fridson, blog of Forbes, 7 March 2014 — Excerpt:

Why is Corporate America holding back on plant-and-equipment outlays?

… Continuing a line of argument dating back to the New Deal, some observers have blamed it all on regulatory burdens and associated uncertainty. One trade publication writes, “Uncertainty over the Affordable Care Act, debate over increase in the minimum wage, and increased government regulations are considered disincentives to business hiring and investing.”

… Attributing anemic capital spending to regulatory uncertainties is unjustified, however, when a simpler explanation is readily at hand. According to the Federal Reserve Board, only 79.2% of productive capacity is currently being utilized. Companies do not typically begin to feel capacity-constrained until that ratio climbs above 80%. It is hardly surprising that with over 20% of their present capacity idle, CEOs are in no hurry to add more.

The ISM survey respondents mention two additional challenges that concern them—slow growth of domestic sales and slow growth of international sales. We can reasonably assume that when sales pick up, factories will operate at a higher rate and companies will increase their capacity. Jumping the gun, on the other hand, would create even more idle capacity. That would likely depress prices and hurt profit margins.

(c) “The cap-X Factor”, Savita Subramanian et al, BofA – Merrill Lynch, 11 March 2014 — Excerpt:

The average age of US private non-residential fixed assets is currently 15.9 years — the highest since 1965. Breaking this down into its components, the average age of structures (power plants, hospitals, restaurants, etc.) is 22.2 years.

This is the highest since 1964, and implies that the average structure was built in 1992, the year that the European Union was formed and the first text message was sent. The average age of equipment (computers, medical equipment, machinery, airplanes, etc.) is 7.4 years (highest since 1995) and the average age of intellectual property products (software, research & development, etc.) is 4.4 years (the highest since 1983).… For most sectors outside of Energy and Financials , in 2010 capital investment dropped to a level that failed to even keep up with depreciation & amortization (D&A) , as shown in Chart 18 . Typically, capex trends well above D&A for two reasons:

- D&A is based on historical cost and is not adjusted for inflation, and

- capex includes both growth and maintenance capex.

Capex/D&A has since recovered, but at 1.2 it remains well below the historical average of 1.4, suggesting that companies remain hesitant to invest in growth.

(d) “The capex call“, Cardiff Garcia, Financial Times Alphaville, 28 March 2014 — Reviewing the numbers and the trends. Excerpt:

Like other parts of the US economic recovery — housing, the labour market — capital expenditures by companies have been a letdown recently, even accounting for the weather. … But capex has been disappointing for more than a year. The growth rate of investment in both equipment and structures declined last year after a strong 2012, which economists credit partly to a one-off tax incentive that pulled investment forward in time.

… Here are the reasons given for the anticipated gains, with a few caveats of our own tacked on at the end …

The mystery of stagnant investment remains, well, mysterious. Net business investment has peaked lower (as a share of GDP) in each successive recovery since the 1980s.

Profit margins remain stubbornly wide, while revenue growth is projected to slow further this year. If companies become nervous that wage growth, whose mildness has been largely responsible for the rebound in profits, will climb without offsetting expectations of higher sales, they’ll become even more loathe to either hire or invest in new equipment.

(3) For More Information

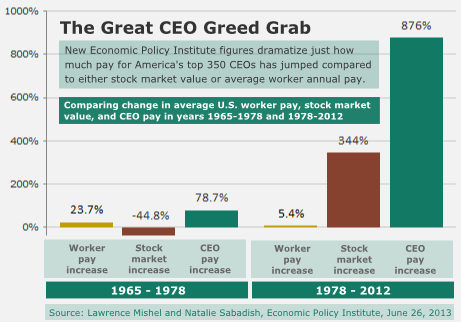

(a) About CEO pay:

- “CEO Pay in 2012 Was Extraordinarily High Relative to Typical Workers and Other High Earners“, Lawrence Mishel and Natalie Sabadish, Economic Policy Institute, 26 June 2013

(b) Other posts about capital expenditures:

- Why America’s growth is slowing, and a solution, 28 January 2013

- Portraits of a nation in decline. An unnecessary and easily fixed decline., 14 February 2013

- Four graphs showing a nation in decline. An unnecessary and easily fixed decline., 1 November 2013

.

.

.

.

Pingback: Watch corporations strip-mine their future (and ours) | AHC-Exchange.com

This is what we need to hear more of. It isn’t just the people at the bottom getting screwed. It is the small investor owners of these corporations. While they have the power via the right to elect the directors, they lack the organization to do so. The white knights COULD BE the activist investors, like Icahn and Ackerman who control large sums and can control significant portions of the shareholdings and wage proxy fights, but they end up being even more interested in short term fixes, than long term sustainability.

Meanwhile, many of these officers spin off or sell the best parts of these corporations to them selves or their buddies and leverage up the remainder and let it go to dust. Check out the history of Castle Cooke(Dole Foods) under David Murdock. I think he now owns all the real estate once owned by the original Castle Cooke.

Probably the best article so far on FM.

However I have a different conclusion, CEO’s and upper management know their companies have no long term future so are cashing out now before the next recession bites.

DaShui,

To say that companies because a recession is coming is absurd. A recession is always coming, and America’s major corporations have withstood many depressions. And two long depressions.

Dashui is not saying that firms are not investing because of an incoming recession (a recurrent event), but because “they have no future” (i.e. because structural factors are bound to make them bite the dust no matter how they invest). Cashing in as soon as possible before a renewed recession reduces the value of the firm is therefore understandable.

Dashui’s statement is interesting, but would require some additional substantiation, especially regarding those conditions preventing US firms to have a future.

By the way, there is an interesting macroeconomic example regarding the lack of investment. Economically, the Communist block appeared to be in good shape during the 1950s and 1960s: at that time, North Korea was doing much better than South Korea, for instance. But civilian investment was being throttled down below replacement levels in favor of investment in military equipment. After the end of the Communist block, the economic situation was revealed in its full extent: lots of very advanced and useless military equipment, with civilian capital — roads and houses, manufacturing and power plants, water pipes and electrical cables — surprisingly old and completely worn out. Nowadays the USA as an economy is refraining from investment in productive capacity while spending huge amounts in futuristic military gear and financial wizardry. How could this go wrong?

Guest,

There is no evidence that US corporations are in u usually weak conditions.

Cash levels are high. Profit margins are at historic high levels. Exports are strong and growing. Leverage levels are above average, but due to extra dinars low interest rates these are easily manageable.

In both domestic and foreign markets US corporations appear to be highly competitive. In fact, exports have been growing for decades in both dollar terms and as a percent of GDP.

The comic says it best. High profits, low employment levels, lousy wages. “Workers don’t share in companies’ productivity gains“, CNN, 7 March 2013.

The profits have come from the chart above — they are wringing the last drop of blood from the middle class. The big companies pay back dividends because their business model is based in how money was made in the past. They make profits now, but since the middle-class isn’t growing their natural market is shrinking. . So they can’t build more factories and sell even more stuff because current customers are tapped out, and the ones with money are dwindling. .

What happens after the middle class is completely strip mined, a forgotten footnote in the history books? What happens then? Where does the growth come from then?

Maybe it gets weird. This is just speculation by me, but could Tesla and Virgin Galactic be the future with products aimed at the super-rich of the planet, expensive toys, space flights. The future profits come from products that target the people who still have the money, the very richest only.

And what about the rest of us? Please excuse this link, really, it’s meant as an indication of decadence and not actual investment advice. “2 Prison Stocks That Look Good: Corrections Corp, Geo Group“, Wall Street Cheat Sheet, 7 April 2014.

from recent thread in (linkedin) IBMers group discussion … including reference that IBM is still using Watson Wyatt, including for IBM “Project Waltz” where court found in favor of the employees.

note the “buyback machine on steroids” is reference to “The Great Deformation” by Stockman

http://www.amazon.com/Great-Deformation-Corruption-Capitalism-ebook/dp/B00B3M3UK6/

also refers to it a form of mini-LBO. This reference has LBO being pioneered by Kravis, one of the founders of KKR … a lot more information here

http://www.amazon.com/Buyout-America-Private-Destroying-American-ebook/dp/B002SV37FO/

LBOs got such a bad reputation in the 80s … using junk bonds for lot of the LBO financing (and major factor in the S&L mess), that in the early 90s they change the industry name to “private equity” and junk bonds became “high-yield bonds”. In the 80s, Gerstner had won the competition to be the next CEO of AMEX. Then AMEX was in competition with KKR to do LBO of RJR and KKR won. However, KKR ran into trouble with RJR and hired Gerstner away to fix it. The IBM board then hired Gerstner away to “resurrect” IBM … where a lot of private equity/LBO techniques were applied. After leaving IBM he went to heading another large private-equity firm, Carlyle. A lot of what is going on in IBM now is still typical of a LBO operation.

Typical LBO operation is to heavily load the corporate with debt for payouts in dividends and stock buybacks (one of the many ways they plunder and suck value out of a company). This has reference that over half corporate defaults are corporations currently or formally held by private-equity.

http://www.nytimes.com/2009/10/05/business/economy/05simmons.html?_r=0

One could make some analogy with Sherman’s scorched earth campaign as they move through US corporations.

http://en.wikipedia.org/wiki/Scorched_earth

and another area is employee retirement

http://www.amazon.com/Retirement-Heist-Companies-American-ebook/dp/B003QMLC6K

some ibm specific:

http://www.ibmemployee.com/RetirementHeist.shtml

from above:

IBM couldn’t just pull the plug on the subsidy, because pension law doesn’t allow a company to take away a benefit a person has already earned or take away a pension right or feature the company has granted. “So we had to design something different,” Sauvigne said. Enter Louis V. Gerstner Jr., IBM’s new president. He’d headed RJR Nabisco in 1993 when it faced a similar dilemma: how to reduce pensions and remove the retirement subsidy without obviously violating the law or provoking an employee backlash. Gerstner and IBM turned to Watson Wyatt, the same consulting firm that had helped Nabisco solve its pension problem.

… snip …

Many of the details are beyond my grasp, but… does this not sound, overall, like a replay of Enron?

The “smartest guys in the room” conclude that working to deliver actual value to customers in a competitive marketplace is a suckers’ game; so they figure out how to make money with smoke and mirrors, laughing at the thought of caring who gets hurt along the way and reassuring themselves that by the time the shit hits the fan, “I’ll be gone, you’ll be gone.”

When do we figure out that that’s not “modern free-market capitalism,” it’s just good old-fashioned fraud?

Coises,

I consider that a gross exaggeration, on several levels. But first, it displays the western tendency to see social dynamics in binary terms, good vs evil. That is seldom so.

It is clearly not “fraud”, as every detail is public, discussed in countless Wall Street reports.

It is a shift in emphasis. Nothing goes to zero, no abandonment of “delivering value to customers.”

Principal-agent conflicts are at the heart of any professional relationship. I believe that we see a systemic deterioration of this balance across American society.

Lawyers exploit the law to benefit their profession.

Doctors exploit their control of medical spending to enrich themselves (e.g., unnecessary surgery, unnecessary tests in docter-owned equipment).

Scientists exploit their role as experts to sound alarms that gain funding for their field.

And CEOs exploit their position for personal gain.

These are all subtle changes in emphasis — of degree– in pre-existing processes , not the eruption of Evil into Eden.

Thank you for the correction. This is an area I know little enough about to misread what is written.

“Principal-agent conflicts are at the heart of any professional relationship. I believe that we see a systemic deterioration of this balance across American society.”

I am, apparently, naïve. I had always believed that at the heart of any professional relationship is the competence and self-discipline of the professional to understand and pursue his or her clients’ best interests, and the clients’ trust that the professional will do that.

Perhaps that partially explains why I see betrayal where you see deterioration of balance.

Do you see a cause for this deterioration? That is, has something changed (some new incentive appeared, or some stabilizing mechanism failed) since some past, better time? Or is this a process endemic to human societies, which proceeds until they reach a discontinuity of some sort?

Head of CFTC suggests regulating CDS … and is quickly replaced. The new head prevents any action in CDS while her husband in the senate gets legislation that would prevent it, she then resigns and joins the ENRON board and audit committee. Her husband was also the major player in getting Glass-Steagall repealed and on Time’s list of 25 people responsible for the financial mess. Not regulating CDS is characterized as favor to ENRON … but law of unintended consequences has “too big to fail” packaging toxic CDOs designed to fail, selling to their customers and then taking CDS bets that they would fail. Estimates of world-wide CDS gambling is between $800T & $1000T.

Passing Sarbanes-Oxley is billed as preventing future ENRON (& Worldcom) and claims that it guarentees executives and auditors do jail time (but requires SEC to do something, however apparently even GAO doesn’t think SEC is doing anything and starts doing reports of public company fraudulent financial filings … even increasing after SOX … and nobody doing jail time)

Gramm and the ‘Enron Loophole’

http://www.nytimes.com/2008/11/17/business/17grammside.html

Phil Gramm’s Enron Favor

http://www.villagevoice.com/2002-01-15/news/phil-gramm-s-enron-favor/

Greenspan Slept as Off-Books Debt Escaped Scrutiny

http://www.bloomberg.com/apps/news?pid=newsarchive&refer=home&sid=aYJZOB_gZi0I

somewhat related to my upthead post awaiting moderation, this is getting a lot of play recently “Capital in the Twenty-First”

http://www.amazon.com/Capital-Twenty-First-Century-Thomas-Piketty-ebook/dp/B00I2WNYJW/

and

http://www.nybooks.com/articles/archives/2014/may/08/thomas-piketty-new-gilded-age ..

http://billmoyers.com/2014/04/18/reactions-to-capital-in-the-twenty-first-century/

An Indictment of the Invisible Hand”

http://www.truth-out.org/news/item/23178-an-indictment-of-the-invisible-hand

from above:

Now, that’s changed again. Capital is rising to its old levels, what Piketty calls the patrimonial state, epitomized by Britain in the first two thirds of the 19th century. As capital rises, the rich simply get richer, and inequality soars. They own the capital, after all, and reap its rewards. And in America, this has mostly been a function, Piketty calculates, of outsize remuneration for CEOs and other managers, who get huge stock options. Their compensation has risen with the stock market.

… snip …

There have been several past references that recently the ratio of avg top executive compensation to avg worker compensation had exploded to 400:1 after having been 20:1 for a long time (and 10:1 in much of the rest of the world).

The Board receive less blame than I think they should also.

And the shareholders. So many shareholders are non-active indexes held by retirement funds whose participants probably don’t even realize they own a part of the company, but wouldn’t know what to do about it even if they did realize, and so they have very little influence on the incentive to engage in a more sustainable long-term strategy.

In my opinion, it’s the separation between those who make the decisions and those who suffer the consequences, combined with the extraordinarily competitive culture of the US’s financial and business centers, that causes individuals at the top to prioritize numbers over people.

Pingback: Listen to the Slowing US Economy … | Bill Totten's Weblog